Bitcoin may have introduced the world to Blockchain technology but the decentralized digital ledger concept is poised to be the next big thing -- all by itself.

Blockchain is the latest technology buzzword. And while blockchain is deeply rooted in the history of Bitcoin, blockchain is not Bitcoin. In fact, blockchain is its own stand-alone technology and is quickly disrupting digital transformation. Let’s take a look at the history of both and see why they are different.

What Is Bitcoin?

Bitcoin is a cryptocurrency, or unregulated digital currency, created and held electronically. No one controls the currency or sees it — it is decentralized, so no person, institution or bank holds it. Bitcoin was first introduced in 2008, when “Satoshi Nakamoto” (the name is widely believed to be a pseudonym) published a white paper titled “Bitcoin: a Peer-to-Peer Electronic Cash System.”

Bitcoin can be used to buy things. In that sense, it is like conventional dollars, euros or yen, which are also traded digitally. Bitcoin’s most important characteristic, however, and what differentiates it from conventional money, is it is decentralized. No single institution controls the bitcoin cryptocurrenty. This puts some people at ease because it means a large bank can’t control their money.

However, Bitcoin is controlled by a transactional ledger that is based on the functional operating system called blockchain technology.

What Is Blockchain Technology?

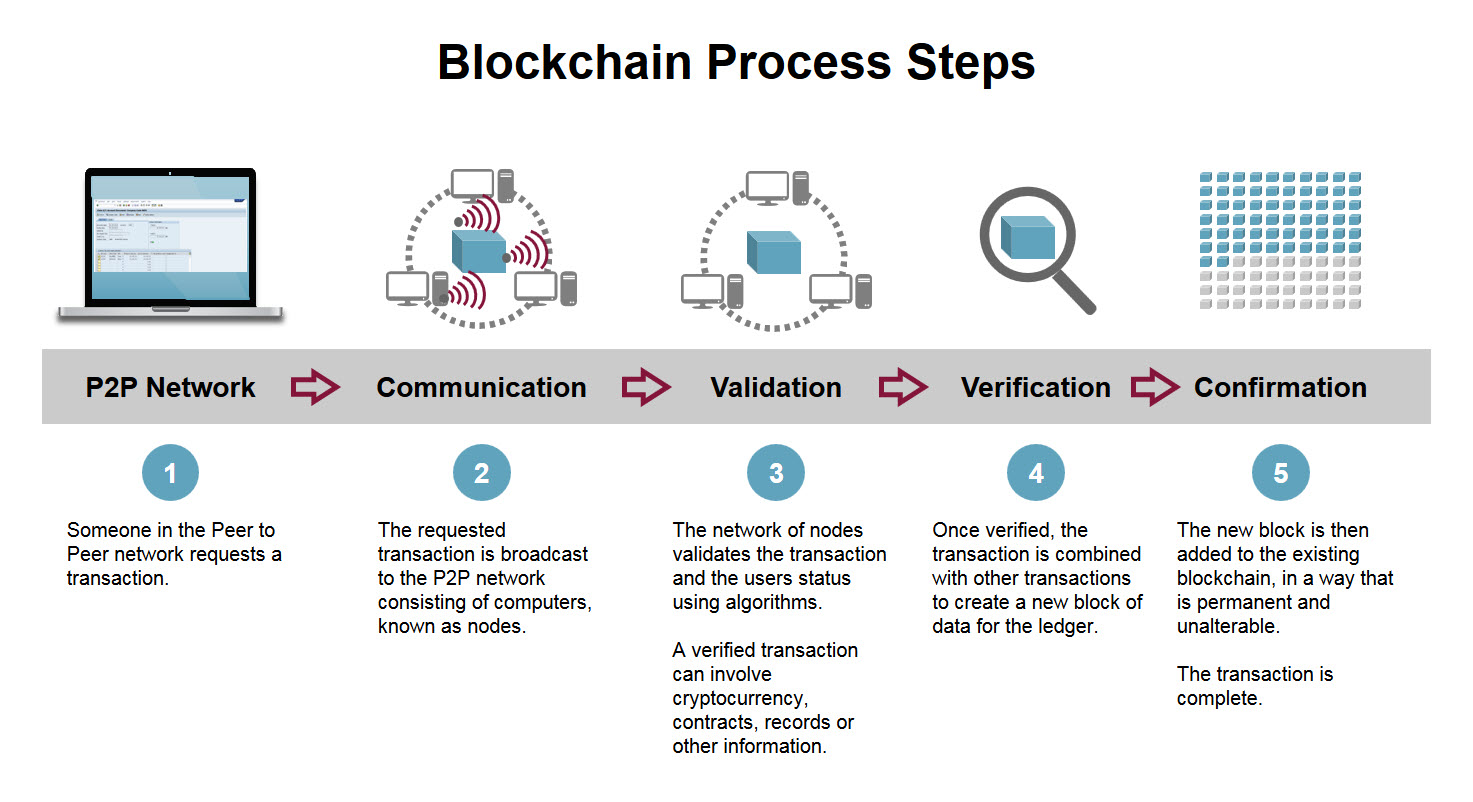

Blockchain technology is a type of distributed ledger that provides a decentralized transactional database, or so-called “digital ledger of transactions” that is shared by everyone on the blockchain network. Think of it as a shared database that users must confirm, verify and record, in which each data block has a logical relationship to all previous data blocks. It is almost like Google Docs on steroids. On the blockchain, transactions are recorded chronologically, and each block becomes an unchangeable locked historical record that is linked to previous and future blocks or transactions.

While the most recent uses of blockchain technology are closely tied to cryptocurrencies (such as Bitcoin), the applications of improving efficiency, automating transactional processing and simplifying reconciliation for banking, insurance, healthcare and supply chain management are endless. The challenge, as we will see here in our next post, is for these industries to abandon their reservations and dive in.